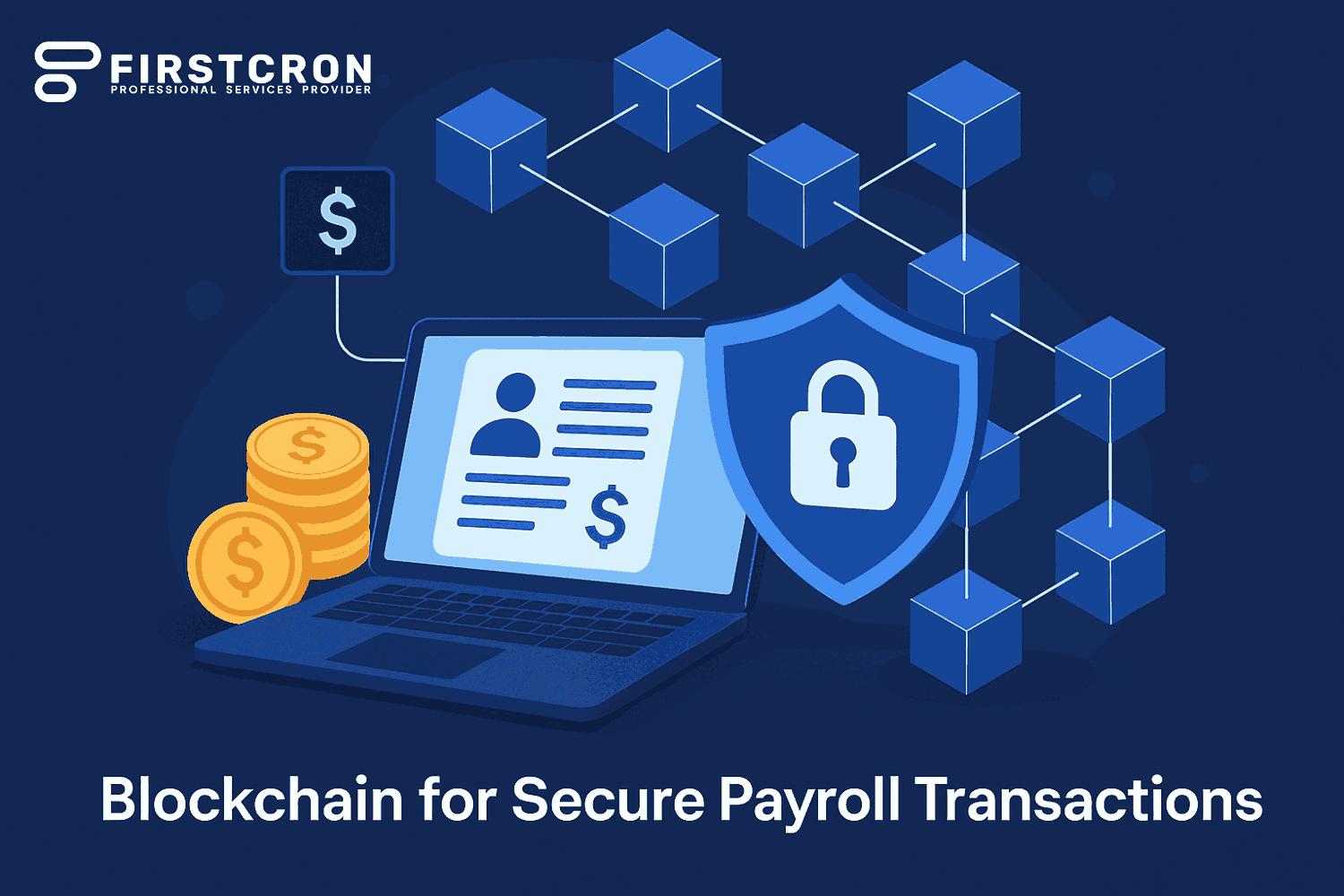

Payroll is one of the most critical functions within any organization, ensuring that employees are compensated fairly and on time for their work. Despite its importance, payroll has historically been a complicated process that involves multiple intermediaries, compliance checks, and financial institutions. Errors in payroll processing not only cause dissatisfaction among employees but also expose companies to regulatory risks and reputational damage. Moreover, in a globalized business environment, companies increasingly employ international teams, making cross-border payroll even more difficult with currency conversions, differing taxation rules, and long settlement times. These challenges demand a system that provides transparency, security, and efficiency. Blockchain technology, with its decentralized and immutable ledger, offers an ideal solution to transform payroll into a more secure, accurate, and streamlined process.

In this blog we’ll cover

- The Fundamentals Of Blockchain In Finance

- Security As The Primary Advantage

- Streamlining Cross-Border Payroll

- Smart Contracts And Payroll Automation

- Enhancing Compliance And Auditing

- Employee Trust And Transparency

- Cost Efficiency For Employers

- Challenges And Limitations Of Blockchain Payroll

- Future Outlook Of Blockchain In Payroll

- Conclusion

The Fundamentals Of Blockchain In Finance

At its core, blockchain is a distributed ledger system that records transactions across multiple nodes in a network. Unlike traditional databases, which are controlled by a single central authority, blockchain is decentralized, ensuring that no single party can manipulate or alter the records once they are confirmed. Every transaction is verified by consensus mechanisms, timestamped, and stored in a block that is linked cryptographically to the previous one, forming a secure and immutable chain. In the context of finance, this technology has already demonstrated its ability to improve the integrity of transactions, reduce fraud, and minimize the need for intermediaries. Extending these benefits into payroll management means that organizations can leverage blockchain to create a system where payments are secure, auditable, and resistant to tampering, while employees can have greater trust in the accuracy of their pay.

Security As The Primary Advantage

One of the most pressing concerns in payroll is the protection of sensitive employee data, including salaries, tax details, and banking information. Traditional payroll systems store this information in centralized databases, which are attractive targets for cybercriminals. Data breaches can lead to identity theft, financial losses, and a breakdown of trust between employers and employees. Blockchain addresses this by decentralizing the storage of payroll data and securing it with cryptographic encryption. Each transaction is immutable, meaning it cannot be altered once added to the chain, and every participant in the system can verify the transaction without exposing sensitive details. This transparency ensures that fraud is nearly impossible, while the cryptographic protection guarantees the confidentiality of employee data. In an era where cybersecurity threats are on the rise, blockchain’s architecture offers payroll systems a fortified defense against malicious attacks.

Streamlining Cross-Border Payroll

The rise of remote work has led to companies employing talent from across the globe, but paying international employees remains one of the most significant hurdles in payroll. Traditional cross-border payments involve multiple intermediaries, high transaction fees, delays in settlement, and complications with fluctuating exchange rates. Blockchain can eliminate these inefficiencies by enabling direct peer-to-peer payments using cryptocurrencies or stablecoins tied to fiat currencies. Such transactions occur almost instantly, with lower costs compared to conventional wire transfers, and are not dependent on banking hours or international clearing systems. This makes payroll more reliable for global teams, ensuring that employees are paid promptly regardless of location. Employers, in turn, benefit from reduced operational costs and the ability to expand their workforce internationally without worrying about the inefficiencies of conventional banking systems.

Smart Contracts And Payroll Automation

Perhaps one of the most revolutionary features of blockchain for payroll is the use of smart contracts. These are self-executing contracts with the terms of the agreement written directly into code. In payroll, smart contracts can automate the release of salaries, bonuses, and deductions based on pre-defined conditions. For example, once an employee has completed a set number of hours or achieved certain performance targets, a smart contract could automatically trigger the payment process. This reduces human error, eliminates delays, and ensures that payroll is executed fairly and transparently. Moreover, smart contracts can embed compliance rules, such as automatic tax deductions and contributions to pension funds, reducing the burden on payroll administrators and ensuring that organizations remain compliant with local laws.

Enhancing Compliance And Auditing

Compliance is one of the most challenging aspects of payroll, especially for multinational organizations that must adhere to varying labor laws and tax regulations. Traditional payroll audits involve time-consuming manual reviews, which are not only costly but also prone to errors. Blockchain simplifies auditing by providing a transparent and immutable record of every transaction. Auditors can trace each payroll entry from initiation to execution, ensuring accuracy and compliance. Regulators can also access blockchain-based payroll systems with permissioned access, allowing them to verify compliance in real time rather than relying on periodic reviews. This not only strengthens regulatory trust but also saves organizations significant time and resources that can be redirected to more strategic initiatives.

Employee Trust And Transparency

Employees often feel disconnected from the payroll process, relying on payslips and bank notifications to verify that they have been paid correctly. Disputes regarding late payments, incorrect deductions, or miscalculations can erode trust and lower morale. Blockchain introduces a new level of transparency where employees can directly view the immutable record of their transactions, including gross pay, deductions, and net salary, without compromising confidentiality. This visibility reassures employees that their compensation is handled accurately and honestly. By empowering employees with access to transparent payroll records, organizations can foster greater trust, engagement, and satisfaction across their workforce.

Cost Efficiency For Employers

Traditional payroll systems involve multiple intermediaries such as banks, clearinghouses, and payment processors, all of whom add costs to the process. In addition, manual interventions, compliance reviews, and audits further increase expenses. Blockchain significantly reduces these costs by cutting out intermediaries and automating processes through smart contracts. Cross-border payments, which traditionally carry high fees, can be executed at a fraction of the cost using blockchain-enabled solutions. For employers, this means a leaner payroll operation with fewer overheads, allowing resources to be redirected towards innovation and growth. Over time, the cost savings from blockchain adoption can be substantial, making it an attractive option for both small businesses and large enterprises.

Challenges And Limitations Of Blockchain Payroll

Despite its numerous advantages, blockchain adoption in payroll is not without challenges. One major hurdle is regulatory uncertainty, as governments across the world are still developing frameworks for blockchain and cryptocurrency usage. Employers must navigate these evolving regulations to ensure that blockchain-based payroll remains compliant. Another limitation is scalability, as blockchain networks can experience slower transaction speeds during high-volume activity, which could affect large organizations with thousands of employees. Integration with existing financial systems also poses challenges, as traditional banks and payroll providers may not yet fully support blockchain solutions. Furthermore, the volatility of cryptocurrencies may create concerns about using them directly for payroll, though stablecoins are emerging as a promising alternative. These challenges highlight the need for careful planning, robust technological infrastructure, and collaboration with regulators to ensure successful implementation.

Future Outlook Of Blockchain In Payroll

The integration of blockchain into payroll systems is still in its early stages, but the potential for growth is immense. As more companies adopt blockchain solutions, standards and best practices will emerge, leading to broader regulatory acceptance and smoother integration with existing systems. In the future, payroll may evolve into a completely decentralized and automated system where payments are instantaneous, global, and secure. Advances in blockchain scalability and interoperability will further strengthen its role in payroll, while innovations such as decentralized identity management could enhance employee verification and onboarding processes. Organizations that adopt blockchain early will not only enjoy the immediate benefits of security, transparency, and cost savings but also position themselves as pioneers in creating a future-ready workforce ecosystem.

Conclusion

Payroll management is a critical business function that demands accuracy, trust, and efficiency. Traditional systems, while functional, are plagued by inefficiencies, security risks, and compliance challenges, especially in the era of globalization and remote work. Blockchain technology offers a transformative solution, bringing unparalleled security, transparency, and automation to payroll transactions. By leveraging smart contracts, decentralized ledgers, and cryptographic protections, blockchain addresses long-standing issues in payroll while preparing organizations for the future of work. Although challenges such as regulatory uncertainty and integration hurdles remain, the long-term benefits of adopting blockchain for payroll are undeniable. As organizations strive to build trust with employees, reduce operational costs, and remain competitive in a globalized marketplace, blockchain is poised to become the cornerstone of secure and efficient payroll systems. For more details please visit firstcron.com.

Tags

Related Post

Navigating Oracle Fusion HCM & Payroll Patch 25C: Key Issues And Solutions For UK Local Councils

July 26th, 2025 10 min read

Learning And Talent Management With Cornerstone OnDemand

October 10th, 2025 17 min read

7 Proven Oracle Fusion Testing Principles To Guarantee Defect-Free Cloud Deployments

May 16th, 2025 15 min read

7 Reasons Why Companies Are Moving From Taleo To Oracle Recruiting Cloud

June 2nd, 2025 14 min read

Navigating Oracle Fusion HCM & Payroll Patch 25A: Key Considerations For UK Local Councils

July 27th, 2025 10 min read

WEEKEND READS

Navigating Oracle Fusion HCM & Payroll Patch 25C: Key Issues And Solutions For UK Local Councils

July 26th, 2025 10 min read

Learning And Talent Management With Cornerstone OnDemand

October 10th, 2025 17 min read

7 Proven Oracle Fusion Testing Principles To Guarantee Defect-Free Cloud Deployments

May 16th, 2025 15 min read

Navigating Oracle Fusion HCM & Payroll Patch 25A: Key Considerations For UK Local Councils

July 27th, 2025 10 min read

UKG (Ultimate/Kronos) — USA And Global, Legacy-to-Modern Workforce Management

October 5th, 2025 23 min read

Driving Compliance And Security With Smart Testing In Oracle Fusion

June 5th, 2025 9 min read

How End-to-End Testing Of Oracle Fusion Enhances Operational Efficiency In Banking

May 23rd, 2025 11 min read

Smart Onboarding Journeys With AI: Personalized Employee Integration Through Oracle HCM Core And Learning

September 13th, 2025 21 min read

Future Proofing Enterprise Testing: The Role Of AI Driven Automation In Oracle Fusion

June 26th, 2025 7 min read